This makes predicting the eventual growth of a fixed annuity a bit more tricky, though they are still more reliable than other types of annuities like variable annuities. Please enter as a percentage but without the percent sign (for .06 or 6%, enter 6). Note that the future value annuity calculator will convert the annual interest rate to the rate that corresponds to the payment frequency. For example, if you selected a monthly payment frequency, the future value annuity calculator will divide the annual rate by 12.

How to Calculate the Present Value of an Annuity

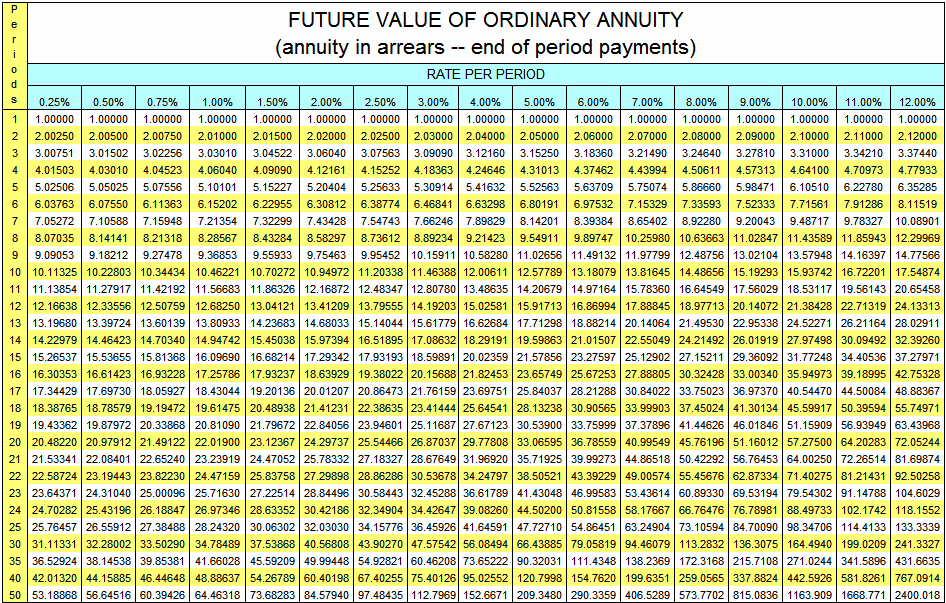

Below the screen, there is a keypad with numerous buttons divided into several rows. The buttons provide various financial calculations and standard calculator functions. The time period between two intervals of an installment is called the future value of the annuity period. As with the present value of an annuity, you can calculate the future value of an annuity by turning to an online calculator, formula, spreadsheet or annuity table. You can calculate the present or future value for an ordinary annuity or an annuity due using the formulas shown below. These recurring or ongoing payments are technically referred to as annuities (not to be confused with the financial product called an annuity, though the two are related).

Future Value of a Growing Annuity (g ≠ i) and Continuous Compounding (m → ∞)

You might also be interested in learning how to calculate the present value of an annuity. If you want to figure out what the annuity might be worth over the course of ten years, use “10” in place of “n” in the formula above. Now that we’ve discussed the basics of annuities, let’s look at how to calculate future value.

Recommended Finance Resources

Use this calculator for financial goal planning and to estimate the returns from regular savings or investments. To put it simply, any financial product that involves a series of payments made at equal intervals is an annuity. The series of payments can be either deposits (with positive signs) or withdrawal (with negative signs). Therefore, if you make regular deposits into a savings account, monthly home mortgage, monthly insurance account or pension plan, you happen to face an annuity. It is possible to roll over qualified retirement plans like 401(k)s and IRAs into annuities tax-free.

Continuous Compounding (m → ∞)

Studying this formula can help you understand how the present value of annuity works. For example, you’ll find that the higher the interest rate, the lower the present value because the greater the discounting. Whether variable overhead efficiency variance the fees are bundled upfront or will be applied over time will depend on the policies of the company issuing the annuity. You should read the fine print on any contract for an underwritten or direct sold annuity.

- Fixed-indexed annuities are potentially more lucrative, but can exhibit some volatility.

- The future value of an annuity refers to how much money you’ll get in the future based on the rate of return, or discount rate.

- Payments from this type of annuity are postponed and are dependent on market conditions so may fluctuate.

- When comparing the future values of Ordinary Annuity and Annuity Due, the primary difference lies in the timing of payments and the subsequent impact on compounding.

In other words, while the index of an index annuity may have a 15% return during a year, the indexed annuity may only payout 10% of returns that year to its investor because of a cap placed on gains. Clearly, there is a tradeoff between added guarantees and receiving 100% of market gains (most variable annuities receive 100%). Unlike fixed annuities, variable annuities pay out a fluctuating amount based on the investment performance of assets (usually mutual funds) in an annuity.

Annuity.org carefully selects partners who share a common goal of educating consumers and helping them select the most appropriate product for their unique financial and lifestyle goals. Our network of advisors will never recommend products that are not right for the consumer, nor will Annuity.org. Additionally, Annuity.org operates independently of its partners and has complete editorial control over the information we publish. The most important way to differentiate annuities from the view of the present calculator is the timing of the payments. If the payment setting is NOT specified in the question, it is assumed that the payments come at the end of the interval.

An indexed annuity, sometimes called an equity-indexed annuity, combines aspects of both fixed and variable annuities, though they are defined as a fixed annuity by legal statute. They pay out a guaranteed minimum such as a fixed annuity does, but a portion of it is also tied to the performance of the investments within, which is similar to a variable annuity. If an index of an indexed annuity doesn’t receive enough positive growth, the annuity investor will receive a guaranteed minimum interest return at the bare minimum. The crediting formulas of indexed annuities generally have some type of limiting factor that is intended to cause interest earnings to be based only on a portion of the change in whatever index it is tied to.

A variable annuity might charge a 9% penalty on funds withdrawn in the first year, an 8% penalty in the second year, a 7% penalty in the third year and so on. Insurance companies apply a surrender charge to a variable annuity contract if the annuity owner withdraws money early. If you’d like to factor in possible surrender charges, look up the variable annuity’s surrender charge schedule and enter the details into the calculator. We insert the values in the future value of the annuity calculator to realize the future value of the present amount. The future value of an annuity is calculated against the number of time intervals.